Robert Kuttner: Introduction

Joseph E. Stiglitz: Deficit Lessons for the Pandemic From the 2008 Crisis

James K. Galbraith: Bad Economic Theory and Practice, Demolished

Heather Boushey: Beware of Austerity Demands Once the Immediate Crisis Passes

Josh Bivens: To Tame Public Debt Without Austerity, Reduce Inequality

Gerald Epstein: Debts and Deficits: What Are the Limits, and Why?

Introduction

BY ROBERT KUTTNER

Deficit phobia is mercifully dead for the duration of the corona pandemic. Along with its devastation of the economy and the public’s health, the crisis has upended the standard economic story about public spending, deficit, and debts.

But austerity economics is one of those zombies that keep arising from the dead. Is deficit obsession really defunct for good?

For now, Congress and the Fed are willing to create almost limitless sums of money to save the economy from outright collapse. A New York Times opinion writer sub-headed his column: “Everyone’s a socialist in a pandemic.”

The macroeconomic counterpart: In an economic collapse, everyone’s a Keynesian.

But what sort of Keynesian, and for how long? That is a hugely consequential question, both for practice and for theory.

At the rate Congress has authorized borrowing to prevent the total devastation of purchasing power, the deficit could easily grow from its current $1 trillion to $3 or $4 trillion dollars this year. If anything, it needs to be even higher.

The obsessively watched ratio of public debt to GDP could rise from its pre-corona level of about 80 percent of GDP to twice that before this crisis is over. What then?

If we review the theory and practice of deficit politics for the past few decades, one category is pure deficit-hawkery, personified by the late investment banker and billionaire influence-monger Peter G. Peterson and his multiple front groups.

In this view, federal deficits and the rising debt load are toxic for the economy because they raise interest costs on the public debt and thereby “crowd out” productive private investments. Peterson and company argued that lower deficits and debts, per se, quite apart from their impact on interest rates, would increase private investment because they would be good for business confidence. Paul Krugman famously ridiculed this view as belief in the “confidence fairy,” who of course never comes.

As a good conservative Republican, Peterson averted his eyes from deficits created by GOP tax cuts. His real target was government spending, especially Social Security and Medicare.

Over four decades, Peterson predicted catastrophe driven by public debts. But when the economy collapsed in 2008, the culprit was private speculative debt; and it was new public debt that kept the collapse from turning into a second Great Depression. Other nominal deficit hawks in the business elite suddenly suspended their concerns, as long as government bailout money went to them.

A second category is made up of situational deficit hawks, who consider themselves “neo-Keynesians.” They dominated both the Clinton and Obama administrations, reflecting Wall Street’s capture of both.

In 1993, Clinton agreed to a grand bargain in which he cut the deficit, and in return, Fed Chair Alan Greenspan lowered interest rates, stimulating a boom that became a bubble. So enamored were Clinton and his aides with deficit reduction that they made it a badge of virtue, pushing the budget all the way into surplus by 1999, to the point where serious people worried about how the Fed would conduct monetary policy when all Treasury bonds were retired.

Bush II put an end to those worries with two huge tax cuts, mostly for the rich, pushing public deficits skyward again. In the meantime, events completely undermined the premise of Bill Clinton’s deal with Fed Chair Greenspan—the idea that public borrowing raises interest rates and inflation.

For the past two decades, interest rates have been low and getting lower—and rising deficits don’t seem to affect them. Even before the corona collapse, despite Trump’s trillion-dollar deficit, interest rates on 30-year Treasury bonds were well under 2 percent.

Yet Obama’s economic team was afflicted with the same deficit phobia as Clinton’s. When the collapse of 2008 hit, Obama’s team proposed a stimulus that would be “timely, targeted, and temporary,” almost as if they were embarrassed to propose it.

Worse, by the fall of 2009, when the economy was far from recovery, Obama’s advisers decided it was time to pivot from stimulus to deficit reduction, killing a second stimulus bill passed by the House and incautiously branding 2010 as “recovery summer.” In Obama’s 2010 State of the Union address, he embraced the austerity plan recommended by the Bowles-Simpson Commission, and even used the discredited metaphor of a household needing to live within its means.

In practice, neo-Keynesians are about as Keynesian as neo-liberals are liberal. Their counsel is a watered-down version of true Keynesian economics—what Keynes’s great disciple Joan Robinson called “bastard Keynesianism”—namely, very mild counter-cyclical public spending.

In office, neo-Keynesians have embraced large deficits reluctantly, guiltily, and as a last resort in national emergencies. They have been eager to return to budget balance as soon as possible, even embracing automatic formulas like the so-called budget sequester.

But one lesson of the 2008 collapse is that the Federal Reserve can simply create huge amounts of money by going into financial markets and buying bonds—with no apparent effect on either interest rates or inflation. The Fed camouflaged what it was doing with the antiseptic term, quantitative easing.

That experience has blown away orthodox fiscal and monetary theory. For if the Fed can create massive amounts of money with no ill effects and many beneficial ones, then a lot of received wisdom goes up in smoke.

Since then, neo-Keynesians have writing op-ed pieces rebranding themselves as friendlier to deficits. In March 2019, former Treasury Secretary Larry Summers co-authored an article with economist Jason Furman titled, “Who’s Afraid of Budget Deficits?: How Washington Should End its Debt Obsession.”

If this is a sincere conversion, let’s welcome it. But let’s also be wary that these fair-weather Keynesians will be among the first to call for austerity to pay down debt once the crisis passes, as they did after 2010.

Somehow, when progressive economists call for large deficits to fight a deep recession, or to combat or low wages that co-exist with near-full employment, they are considerd suspect, as unsound leftists. But when a Larry Summers belatedly comes around to that view—a decade late and a trillion dollars short, and without crediting the prescient dissenters—it is a stop-the-presses, Eureka moment.

THOUGH THERE WOULD seem to be a consensus on the need for very large deficit spending, there really isn’t. For the really interesting part of the debate concerns how big deficits can be, for how long, and for what purposes.

Modern Monetary Theory, for instance, holds that the capacity of government to borrow and a central bank to create money is virtually infinite. The capacity is especially large at a time when the economy has collapsed and there are good uses for that money.

If the economy ever reaches full capacity to the point of generating inflationary pressures, that would be the time to start pulling back. But until then, full speed ahead.

MMT has evolved. In its current incarnation, the proposition that government can create unlimited amounts of money until the economy hits capacity constraints doesn’t apply everywhere, but only to nations that can borrow in their own currencies.

If Argentina tried to follow MMT, for instance, the result would be massive inflation and a run on the currency. One policy question is how the rules of the global system disadvantage smaller, dependent nations—and how they might be revised so that such nations would have the same MMT policy options available to the U.S.

Other, broader questions for economists of all stripes, now embracing massive deficits include these: Is one dollar of fiscal stimulus as good as another? Is public borrowing to replace lost paychecks the same, macroeconomically, as borrowing money to bail out hedge funds?

Is a tax cut as good as public investment? If not, why not? In terms of stimulus, does it matter whether a tax cut goes to the rich or the poor?

It’s an old argument. In 1962, when President John F. Kennedy proposed a stimulus, his chief economic adviser, Walter Heller, wanted it in the form of a tax cut. John Kenneth Galbraith, a left Keynesian, argued for more public spending, both on grounds that America’s public household needed the money and because every dollar would be spent; hence public investment would be more stimulative.

Heller won, more on political grounds than economic ones. Everybody loves a tax cut; not everybody loves public spending.

One other issue divides conservative economists and different stripes of self-described Keynesians: what to do when the current crisis ends. Suppose the legacy of all this public spending is a debt of 200 percent of GDP? Is that a problem? Do we need to go on an austerity kick to bring the debt ratio down, at the risk of reducing economic output and increasing unemployment? Or are there even more public needs that justify more public borrowing?

A final issue concerns what amounts to a blurring of fiscal and monetary policy. In standard economics, fiscal policy refers to taxing, spending, borrowing, and budget surpluses or deficits. Monetary policy refers to interest rates and the availability of credit. But if the Fed just creates money by going out and buying bonds, is that fiscal or monetary policy, and does it matter?

We put these questions to several economists of different persuasions. Their comments follow.

Deficit Lessons for the Pandemic From the 2008 Crisis

BY JOSEPH E. STIGLITZ

Economics is sometimes defined as the science of scarcity. If resources are scarce, it would seem, a country can’t print money, give it to someone, without consequences: There will be inflation, and those receiving the money will get resources at the expense of others. But Keynes put the lie to this reasoning, pointing out that often the economy is not using all available resources, and giving more purchasing power to some individuals may result not in inflation, but in higher levels of production and prosperity. Keynes was right, but left a number of questions unsettled: how do we know when all resources are fully utilized? Is there a clear demarcation? Will inflation set in while there may still be some underutilized resources?

In the subsequent decades we thought we had learned the answers: As resources get “tight,” inflation increases—and will even accelerate, as people come to expect more inflation. Sufficient expansion of the monetary base and large deficits will lead us eventually into such inflation.

But the new millennium has not been kind to this consensus view of orthodox macroeconomics. There appears no stable relationship between the slack in resource utilization (measured say, by unemployment) and inflation. And the massive expansion of the base money supply and the accompanying low interest rates after 2008 did not lead to inflation. In some parts of the world, the fear was, instead, deflation.

But some have learned the wrong lesson from these experiences. At least part of the reason that there was no inflation was that the banks that had access to these funds didn’t lend them out: With no demand from consumers and firms, of course, there was no inflation. Monetary policy was both ineffective and non-inflationary. But that outcome was because of the way that we distributed the money. If we had had “helicopter money,” raining dollar bills on poor Americans, I feel confident we would have a quicker recovery; and if we had a large enough helicopter downpour, we would have had inflation.

How inflationary any expansion of money or increase in the deficit is thus depends on how the money is spent. If it goes to finance investments, aggregate supply will eventually increase. But the increase in demand and in supply may not move in tandem: If before the increased public investment, resources were fully used, there could be a period of inflation, followed by a period in which inflation is lower than it otherwise be.

The notion that expanding deficits necessarily lowers private investment is just wrong. As is the notion that we can ascertain the effects of monetary policy on inflation by just looking at the interest rate (real or nominal). If policy expands aggregate demand, it will enhance businesses’ willingness to invest. And if monetary policy expands the availability of credit, say to small and medium sized enterprises, it will enhance their ability to invest. But obviously, if we give the banks free reign—to create a housing bubble, to finance speculative investments, and to engage in others forms of mischief—looser monetary policy may not result in more investment. There may be more effective ways of stimulating investment than just relying on monetary policy—such as investment tax credits. And even if there were some crowding out—so an increase in the deficit to finance an increase in public investment resulted in less private investment—the increase in long-starved public investment may be far more productive, with far higher returns, so national income may still go up.

This crisis presents a particular challenge. The underlying problem is not an insufficiency of aggregate demand; that’s why referring to the bill that Congress passed as a stimulus bill is a misnomer. The problem is that the virus has led to social distancing—undermining both demand and supply. In addition to trying to protect our health, the spending was directed (at the insistence of the Democrats) to protecting the most vulnerable. We were on target for a deficit of 5 percent of GDP; now it looks like three times that or more—a new record.

To me, there is little doubt that in the absence of this deficit spending, not only would there be enormous suffering today, but our economy’s revival would be imperiled. There is a chance we would have been in a financial gridlock—or worse. Households and firms couldn’t pay their creditors and landlords, leading to a bottom-up bankruptcy cascade—the opposite of the top-down trauma our economy went through in 2008, and far harder to deal with. The recovery may still be difficult: Firm and household balance sheets will have worsened; despite the help, some firms will go bankrupt—and won’t be un-bankrupted once the pandemic passes. Provision of liquidity will help, but there will be many facing solvency problems, and aggregate demand may still be tempered. But if we have succeeded in getting large amounts of money into the pockets of ordinary Americans, eventually, this money will be spent. And the coronavirus has, at the same time, resulted in a marked reduction in supply, at least for the duration of the pandemic. One can’t help but think that eventually the imbalance of demand and supply might have consequences.

But I’m not particularly worried (or I wouldn’t be if I had confidence in our economic leadership.) First, before the crisis, it was clear that there was at least some slack in the economy. Secondly, recent evidence is that when inflation increases, it does so only slowly, and that gives us time to respond. We could reverse the tax cuts for corporations and billionaires of 2017. We could move towards a fairer tax system, by taxing the returns to capital, including capital gains, at least the same rate that we tax workers. We could tax pollution and other negative externalities. In short, if and when there is evidence of excess demand, we can take countervailing measures.

After the pandemic is conquered, we’ll still face two other crises: our inequality crisis and our climate crisis. Addressing each of these will require significant increases in government spending. We need to retrofit our economy, for instance, through “green infrastructure.” If we had to have a larger deficit to save the planet, the choice should be a no-brainer. But moving towards a greener economy, even financed by deficits, will lead us to a more robust and more innovative economy—and as we’ve learned time and time again, that could even lead to lower deficit.

One might have hoped that the silver lining of this pandemic is that we have gotten over our debt obsession. But I’m worried that it may return. Paul Krugman talks about “zombie ideas”—ideas that have long been discredited, but nonetheless continue to have sway among the living. I’ve discussed two of these zombie ideas: that deficits are necessarily inflationary and crowd out private investment. A third zombie idea, related to these two, is that deficits beyond a certain level (say 80 percent of GDP) are bad for economic growth.

That was an idea popularized by Harvard Professors Ken Rogoff and Carmen Reinhardt, based on a paper that was thoroughly discredited by a graduate student from UMass Amherst. While he called attention to the “spreadsheet error,” others before and after had talked about some of the deeper econometric and theoretical fallacies. There had been no test of the statistical significance of the difference in growth rates associated with higher levels of debt. There was no test of causality—was it that countries that were having deep structural problems which led them to grow more slowly wound up having more debt? Low growth led to high debt, not the other way around. There was no examination of how the debt was created, what the money was spent on, who got it, which our analysis above suggested was crucial. And it was totally ahistorical: At the end of World War II, both the U.S. and the U.K. had very high levels of debt, yet the period after the war was the fastest period of growth. And with that fast growth, the debt-to-GDP ratio rapidly came down.

Of course, if one uses a high debt-to-GDP ratio as an excuse for austerity, and, as is typically the case, austerity leads to slow growth, then there will be an association between debt and low growth. But that association is a result of the misguided policy advice coming from these deficit hawks. Their false narrative has had consequences—it has led to low growth. It wasn’t the laws of economics that led to these adverse outcomes; it was bad economic analysis, and bad policy.

This lesson is of particular importance as we emerge from the pandemic. There will be those who look at the large increase in the debt-to-GDP ratio and saw we need another dose of austerity. It will be used as an argument to cut vital public investments and social protection programs—including expenditures that would make us better prepared to meet the next health, economic, or societal crisis. We should steel ourselves for the coming battles: Deficits for tax cuts for billionaires and corporations—and for massive corporate welfare—are one thing; social expenditures and public investments are another. Of course, these deficit hawks have gotten it exactly wrong. And that’s where the political battle will lie.

Joseph E. Stiglitz is university professor at Columbia University, co-recipient of the 2001 Nobel Memorial Prize in economics, and former chairman of President Clinton’s Council of Economic Advisers. His most recent book, People, Power, and Profits: Progressive Capitalism for an Age of Discontent, comes out in paperback this month.

Bad Economic Theory and Practice, Demolished

BY JAMES K. GALBRAITH

The corona crisis has obliterated, one hopes for all time, certain shibboleths of the economic textbooks and the Congressional Budget Office. Among these, especially, are crowding out, deficit and debt thresholds, and the natural rates of interest and unemployment. If the pseudo-Keynesian notion of “stimulus” and the habit of relying on debt and stock booms to drive growth can also be buried under the avalanche, our chances of surviving the aftermath will improve.

In the United States, 3.3 million workers filed for unemployment insurance two weeks ago—about five times more than in any previous week in history—and then 6.6 million filed for unemployment last week. That number will keep rising. Gross domestic product will crash this quarter—perhaps by more than ever before. These events are measures of the effectiveness of the lockdown. They are also a sign of the fragility of what was there before, and the difficulty—the impossibility—of going back to the world that existed before this pandemic.

With spending soaring and taxes collapsing, deficits could rise to 20 percent of GDP this year or even more—a number without parallel since the vast mobilization of World War II. But this is a good thing. Nor is any sane person worried about interest rates: They are near zero, and they will be there indefinitely. Crowding out, the notion that private investment will be deterred by public deficits, has been debunked by catastrophe. Anyone still teaching such ideas should be ashamed.

The public debt is net private financial wealth—to the dollar. That is why the stock market went up, not down, just after the big bill cleared the Senate. But the stock rally was a sign of nothing good. Those gains reflected the corporate bailout and measured how much the paper losses of wealthy shareholders are being repaired. That’s a temporary and excess benefit; it will prompt many caught out in the first wave of losses to dump their stocks. Investors know that industries hit early and hardest (among them airlines and aerospace, hotels, and leisure) will not recover from this, at least not in the form they took before this crisis. It’s not just that travel restrictions will endure. It’s not just that people won’t have the money. It’s that even if they do, ordinary customers won’t soon resume old traveling habits while danger appears to lurk.

Anyone who says this new public debt must be repaid later with more cuts to basic services and social insurance is obviously a fool. We’re in this debacle because we listened to such people for far too long. Notoriously, hospital beds per capita in this country are about half what they were 40 years ago, and one-sixth what they are in South Korea. Critical supplies are desperately short. Private health insurance is melting down. The millions thrown off payrolls—unnecessarily—are now faced with the choice of scrambling for bridge coverage, or roughing it uninsured in a pitiless system, while companies are swamped with claims. Meanwhile in the United Kingdom, millions including the Tory Prime Minister, Boris Johnson, stood on their doorsteps to cheer the National Health Service, and medical teams from Cuba and China have set up field hospitals in Lombardy, one of the richest places in the European Union. Do we get this, finally?

Part of the new bill is called “stimulus,” perhaps the most offensively stupid word ever applied to an economic problem, the quick-fix reflex. One such stimulus is already in place: a program of cash rebates through the tax system. The idea is supposedly Keynesian, but it doesn’t come from Keynes: His idea, and Franklin Delano Roosevelt’s was to hire the unemployed and put them to work on useful tasks. In the present situation, the notion of stimulus is especially wrong-headed: The economy cannot use stimulus when all the stores are shut! You do not fight a war by cutting taxes or sending out checks.

Even as a bare-bones system to support people in need, tax rebates are badly flawed. They are based on 2018 (sometimes, 2019) tax returns, which are out of date. Babies are born, weddings and divorces happen, people gain and lose jobs all the time. So the payments will be haphazard, and that will breed resentment. As for those without direct deposit, especially the low-income unbanked, the approach is far too slow. Those folks need paper checks, and because of simple printing bottlenecks it could be weeks or months before the last ones hit the mail. But the poor need food money right now. And those who do not file taxes—because their incomes are too low, or because they are undocumented—get nothing from this anyway. They are still here, they are still at risk, they are doing essential work, and they still need to eat.

Payroll replacement through employers, which has also been proposed by the conservative economist Glenn Hubbard, is much better than a tax rebate and could be put in place instantly for workers not yet laid off. The big bill provides a weak incentive: a 50 percent tax credit for payroll expenses for those staying home, with a cap of $10,000. The credit should be refundable (if it isn’t); it should be bumped up, and banks should be required to make a zero-interest loan to their business customers to cover the float. With a full rebate for 70 or 80 percent of payroll up to $20,000 per worker over three months,, the idled-wage workforce would be decently covered for now. The unemployment insurance system could then concentrate mainly on enrolling self-employed and gig workers, made newly eligible, so that they too can stay home. Unlike the tax rebate scheme, these measures do not (or need not) discriminate by status.

Another fast way to give most households some extra dollars each month is for the government to pay telecommunications companies to cover the cost of basic internet, cable, and telephones. People need to be connected, and they need to stay indoors. Giving them that much for six weeks or two months is not big money, but in a low-income household it will matter, and it could be done overnight. This idea is also non-discriminatory.

However money is distributed, there is a crucial need to keep a balance between purchasing power and the very limited range of goods for sale. The danger is that extra income may fuel panic buying, shortages, and profiteering. Stores are already limiting purchases of essentials per shopping trip, but that will not defeat a determined profiteer. If big black markets develop, social distancing will break down. So if community spirit and informal rationing does not hold—and it may yet!—then wartime measures of rationing and price control must be imposed. Whatever it takes, for as long as it takes, the supply chain must hold out.

There is another danger to supplies, which is that critically-needed workers in the most exposed positions may at some point just quit their jobs. This can happen if too many co-workers get sick. It can happen if the incentives to keep working are not right. Stores cannot function without stockers, checkout clerks, and security personnel. The right solution is to raise those wages and provide protections to these workers, such as masks, gloves, and disinfectant. A stiff emergency-wage supplement for them, full medical coverage, and personal protections with a priority, just after medical staff, should be added to the next bill. Instacart workers are already rightly striking for decent treatment, and their action illustrates just how fragile the supply chain may be.

Most important, as we confront the crisis, people must be safe and secure in their homes. A fast and efficient way to meet that goal is to block evictions, foreclosures and utility stoppages. Water and power must be kept on, and turned back on where it has already been stopped. Debt collections and wage garnishments must be halted. A ban on new homelessness must be absolute and unconditional; collecting mortgage payments, rents, and debts is secondary. People should be able to defer fixed monthly bills if they need the money for food or medicine.

Meanwhile, there are management issues that are just as vital as the economics of social balance. Top priority: The ongoing chaos in medical supplies must be brought under control. Michael Lind and I have proposed a Health Finance Corporation to rationalize the medical supply chain. The Defense Production Act should be ramped up for masks, test kits, reagents, and ventilators—crucial medical supply needs. The supplies now flowing from China are hugely welcome and open up new possibilities for mutual aid and cooperation. The National Guard and the Army can set up field hospitals, as is already happening in New York. Ireland has nationalized all hospitals to ensure equal treatment for all patients. An open-source respirator design for under $500 just emerged in Canada. These and other measures will only support what the health authorities tell us is necessary: a shutdown long enough to break the chain of transmission. They are not there to “stimulate” but to manage a rapid conversion to an economy of social self-defense.

What happens afterwards is a problem for another day. But we already know that some people—the very rich, the very powerful—got an immense bailout from their early losses. A few even got much richer by selling short. Many more have immense losses, both income and wealth, and while their fixed bills may be deferred for now, those debts have not been forgiven. They are piling debt on debt. And just as the public debt now being incurred will never be repaid, the private debts now piling up will be un-payable if income flows continue to flag. In the aftermath, this will translate into easy pickings and fire-sale liquidations of homes, businesses, and land—anything owned by anyone caught in the squeeze. Do not expect this to go down easily.

And those debts, like the vicious circle of war debts and reparations after World War I, will be a vast barrier to economic revival of any sort. So there will be a reckoning later on. That much is already inevitable, and it means a clash between the legal rights of the wealthy and basic interests of a civilized society, let alone a supposed democracy. With the fresh experience of the pandemic, it is not likely that people will tolerate a new round of neoliberal austerity, wealth concentration, and plutocracy; social order will collapse before that. So we’ll need a general reorganization, a new priority to the common good, and a general write-down and reset of the financial system, including perhaps a capital levy and land reform to reset the distribution of wealth.

Fortunately, to come back to Keynes, Versailles and its aftermath are not the only historical example. There is also the model of debt cancellations after World War II, as fiercely advocated by Keynes as he had opposed the Carthaginian Peace in 1919. And this set the stage for the 30-year phase of successful welfare-state social democracy that followed that war.

In short: The pressing needs right now are to provide critical care and to break the chain of transmission of COVID-19, while keeping the population supplied and calm, for as long as it takes to get the job done and build sufficient capacity in the medical system. Compared to these tasks, our economic numbers—and the stale nostrums that used to go with them—do not matter at all.

James K. Galbraith holds the Lloyd M. Bentsen, Jr. Chair in Government/Business Relations at the Lyndon B. Johnson School of Public Affairs, the University of Texas at Austin. He is a member of the Lincean Academy and author most recently of Inequality: What Everyone Needs to Know (Oxford University Press, 2016).

Beware of Austerity Demands Once the Immediate Crisis Passes

BY HEATHER BOUSHEY

The coronavirus is, above all, a public-health crisis, and the economic impact could be devastating. But before any of us even heard of COVID-19, our society and economy suffered from deeply-ingrained problems, starting with economic inequality, which this crisis will undoubtedly exacerbate. The need for substantially increased public spending and investment will not diminish once the public-health crisis fades.

What will diminish is the broad political consensus that made possible the recently approved $2.2 trillion burst of federal spending to support families and businesses during this economic shutdown. Indeed, if recent history tells us anything, that consensus will fall apart once the immediate health crisis dissipates and people can gradually return to work.

That will be another dangerous moment for the country.

First, it’s likely that the economy will be at a precarious tipping point, and the risk of doing too little to support families and businesses will still far outweigh the risk of doing too much. We will need to continue to pump money into the economy if we are going to avoid a coronavirus recession that makes the Great Recession of 2007–2009 a fond memory. Families will continue to need support, as businesses struggle to ramp their operations back up. And states and localities will need to avoid spending cuts, as the crisis decimates their tax revenues. Such cuts would exacerbate hardship for families and undermine recovery.

There was a need for substantially greater public spending before any of us ever heard of the coronavirus: to address pervasive economic inequality, to invest in human, physical, and intellectual capital. That need will be even greater in the virus’s wake.

But deficit hawks—particularly the über alles crowd, who believe that budget deficits are acceptable only when caused by tax cuts—will be out in force, demanding austerity. We got a taste of what’s to come when some members of Congress objected to the $600 weekly increase in unemployment-insurance checks contained in the Coronavirus Aid, Relief, and Economic Security Act, because some low-income workers might receive a little bit more now than they do when they’re working.

Politicians who fretted about short-term work disincentives in a week when more than 3 million people had just been laid off are not going to give a damn about workers a few months from now. So, the rest of us must.

Some of the needs were exposed by the current crisis. For example, we need to permanently, not just temporarily, reform our unemployment-insurance system to cover more workers and increase benefits. There is plenty of room to do that without creating work disincentives. The logic supporting guaranteed paid sick days for workers and families affected by COVID-19 will not go away with the virus. That, too, needs to become permanent policy, and the ridiculous policy of exempting large employers needs to be scrapped. Likewise, the need for accessible, affordable, and quality day care and early childhood education is critical for supporting working families and maximizing labor force participation, especially for women. And certainly, to stave off an even deeper recession, any recovery legislation will need to include temporary additional direct payments to individuals. That is a surefire way of supporting aggregate demand to mitigate and recover from a recession. What’s more, there is a massive, longstanding need to invest in our outdated infrastructure, in our human capital, and our store of scientific and other knowledge. And, of course, this crisis underscores that it is imperative that all have access to health insurance.

The fear of inflation and soaring interest rates that lies at the supposed concern about deficits and spending never seemed more irrational than it has over the past several years. We were already in an era of prolonged low interest rates, partly because of low investment and an aging population. Even when the economy seemed to be flying, with the unemployment rate as low as it had been in decades and jobs continuing to be added each month, the economy was not being pushed beyond its capacity. Even in these seemingly ideal conditions, wages for average workers had only recently begun to budge, after decades of stagnation.

Clearly the financial markets have not been concerned, as investors were still putting their money in U.S. treasuries, keeping interest rates low, even before the coronavirus. Now, rates in inflation-adjusted terms are about as close to zero as they can get, and inflation concerns feel like a distant memory. There’s a huge opportunity cost in failing to spend on critical priorities out of fear of phantom inflation. Deficit and debt concerns should not stand in the way of bold action.

Even if we decide that raising deficits indefinitely is not sustainable, cutting spending will not be the answer. Taxes are the best way to reverse these trends, particularly on corporations and the wealthy. The failure to tax those at the top—not only due to the 2017 tax cuts but also to decades of supply-side tax policies since the 1980s—has contributed to higher inequality. U.S. tax laws lowered federal revenue to only 16.2 percent of GDP in 2018 and 2019, compared with 19.8 percent in 2000 (before President George W. Bush’s tax cuts) and 17.8 percent in 2007 (before the recession). It’s been heartening to see proposals for higher taxes on the wealthy and on corporations from every major Democratic candidate for president, from those on the left to those in the middle.

President Barack Obama’s chief of staff admonished him to never to let a good crisis go to waste. Unfortunately, by turning to austerity in 2009, his administration did just that. As the past decade has shown, austerity was not the answer then, and it surely is not now.

Heather Boushey is the president and CEO of the Washington Center for Equitable Growth and the author of Unbound: How Inequality Constricts Our Economy and What We Can Do About It (Harvard University Press, 2019).

To Tame Public Debt Without Austerity, Reduce Inequality

BY JOSH BIVENS

Robert Kuttner is right that a growing share of economists is (finally) getting more evidence-minded about the effect of public debt. These economists have seen that the large increase in the ratio of debt to GDP in the past decade failed to boost interest rates or inflation much at all. From this they have drawn the correct inference that rapid debt reduction should not be on the short-term priority list. But too few have addressed the question of why growing debt hasn’t pushed up interest rates or debt. This might be because the answer takes one out of politics-free observation: It’s because of rising inequality and the policy failure to stem it.

To understand inequality’s role in breaking the link between rising debt and interest rates or inflation, start with a generally-accepted point: All else equal, rising public debt should boost the growth of aggregate demand (spending by households, businesses and governments) relative to the economy’s productive capacity. But if the last decade’s rise in debt hasn’t budged interest rates or inflation, then the clear implication is that the economy is suffering from a chronic shortfall of demand even in the face of rising debt.

Most economists recognize that demand shortfalls can exist; recessions are just particularly serious demand shortfalls. But a generation of macroeconomists assumed these shortfalls were temporary and easy-to-fix, and that the much more pressing problem that policymakers would have address was a supply shortfall that spurred inflation or rising interest rates. Hence, for example, the Federal Reserve adopted a generations-long itchy trigger finger on interest rate increases to fight potential inflation, keeping labor markets too soft to give typical workers the labor market leverage they needed to spur reliable wage growth.

Some economists have certainly noted that this chronic shortfall in demand is the reason why growing debt hasn’t led to rising interest rates, and this has been a big analytical leap forward. But why this demand shortfall emerged and persists will require more leaps. Two key reasons (if not the only ones) include the policy-driven assault on the labor market leverage of typical workers that has been the root cause of the rise in market-income inequality, and the failure of our tax-and-transfer system to respond to this rise in market income inequality with progressive tax increases or more redistributive spending. These two “whys” are essentially the story of how inequality happened and what fiscal policy did not do to check it.

As inequality rose, more and more income was redistributed to the top, where households save a lot more than their low and middle-income peers. For a while we could maintain demand growth in the face of this steady upward redistribution by lowering interest rates and spending out of the occasional asset-market bubble fueled by private debt. But now we’re firmly in a world where interest rates can’t lift off much beyond zero without sacrificing any serious chance at reaching full employment.

Given this inequality we’ve generated over the past generation of economic life—and the demand shortfall that accompanies it as a result of the higher savings rate of households on the winning end of this rising inequality—the only way to sustain full employment going forward is to rely more on larger federal budget deficits. And if the choice is higher deficits with full employment versus lower deficits without, it’s clear that the best choice is to bring on the deficits. But this also means that anybody determined to slow debt growth needs to come with a plan to lower inequality and hence generate more private-sector demand growth.

Somewhat ironically, one sure policy path that would allow full employment to coexist with smaller deficits would be to increase spending on social insurance and safety net significantly while raising progressive taxes even more. This would result in a smaller deficit, but the progressive redistribution would boost demand growth by more than the slower debt growth reduced it. This path of increasing spending and taxes, leaving government bigger but deficits smaller, would not only be a solid economic strategy, it would also provide a pretty good test for whether it’s the size of the debt or the size (and progressivity) of government more generally that is the real worry for self-professed fiscal hawks.

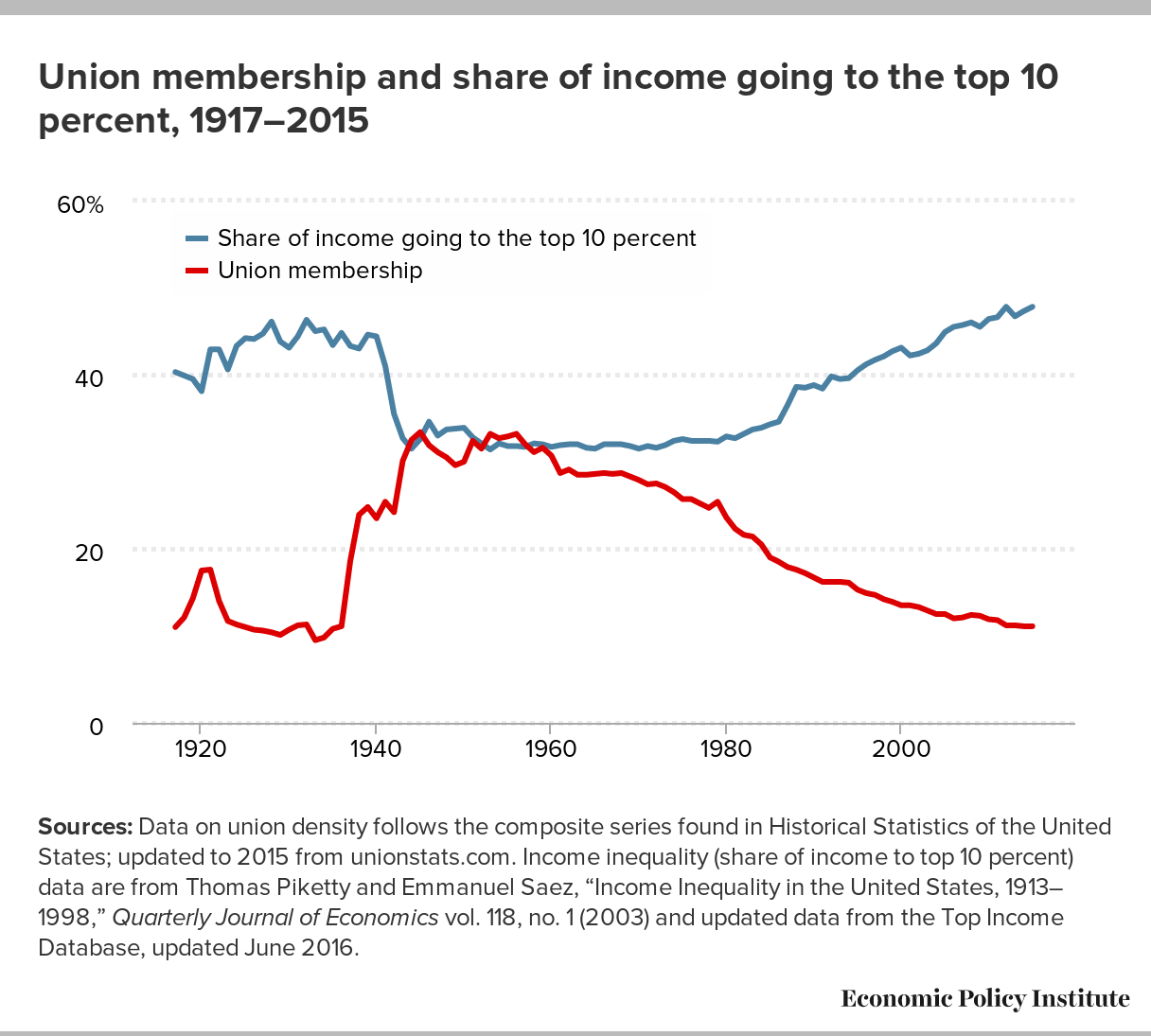

A complementary plan to reduce inequality and hence allow lower deficits to co-exist with full employment is pursuing measures to boost U.S. workers’ leverage in labor markets. On the face of it, restoring the effective right to bargain collectively might not seem like a fiscal issue, but, the assault on this right has had profound effects on American inequality, and it would be far easier to significantly reduce debt ratios while maintaining full employment if this distribution of market income was much more equal. Again, anybody who seriously wants smaller deficits and full employment needs to think about how to reduce inequality—and boosting the labor market leverage of typical workers is a key tool for this effort.

{kind=link}

In the end, discussions about the proper level and trajectory of public debt cannot be divorced from other developments in the economy. There have been historical episodes across countries when economic growth really was constrained by the supply side, and running large fiscal deficits really would have put upward pressure on interest rates or inflation. But growth in the modern and unequal United States has been demand-constrained for at least a couple of decades now. Given this, rising debt not only does no harm, it actively boosts growth.

We should be really clear that the observation that raising debt in our demand-constrained economy is good for growth is not really anything to cheer. In fact, every year that we allow economic growth to be demand-constrained is another year of waste. We know, pretty clearly, how to solve demand constraints: use more debt used to finance demand-generating spending until we finally reverse the huge rise of inequality. But we haven’t yet found the political will to do it, and so the waste continues.

We should also be clear that there is no problem-free world in economic policymaking. Even if we managed to achieve a lot less inequality, faster demand growth and slower-growing public debt, policymakers will face problems, just different ones. For example, the phantom problem of recent decades—upward pressure on interest rates and inflation— would become real. The standard playbook for addressing these problems has been to rely on the Federal Reserve to bludgeon labor markets with higher interest rates and unemployment. We can do much better than that, using bargained wage restraint and incomes policies to slow inflationary pressure. But I would trade the problem of how to control too-fast demand growth for our current demand stagnation in a heartbeat. This trade would at least mean we’ve solved the infuriating political failure that kept us from addressing the easily solvable demand shortfall that has hampered growth for far too long.

Will the recent crisis somehow illuminate a path out of this political failure? It’s possible. At a minimum, the crisis highlights some crucial downsides of weak public investment and social insurance, and, it should have helped many recognize that lots of work that is currently low-wage is extremely high-value. Maybe this is a good start for a new conversation on all these issues.

Josh Bivens is the director of research at the Economic Policy Institute. He is the author of Failure by Design: The Story Behind America’s Broken Economy (EPI and Cornell University Press, 2011) and Everybody Wins Except for Most of Us: What Economics Teaches About Globalization (EPI, 2008).

Debts and Deficits: What Are the Limits, and Why?

BY GERALD EPSTEIN

Recent headlines from The Financial Times:

U.S. taps market for stimulus funds at historically low rates (April 3)

How central banks beat back the ‘bond vigilantes’; unlimited bond buying has made it near impossible for investors to punish overspending (March 31)

Fed sets up scheme to meet booming foreign demand for dollars (March 31)

The toothless inflation peril; price pressures are no reason to pull our policy punches (April 2)

China’s $13tn bond market shines as Treasuries turn treacherous (March 24)

Nothing has gotten the attention of the political and economic establishment like two back-to-back crises with the potential for Great Depression–level economic devastation. The first time around, President Obama, Larry Summers, and the other situational hawks, as Kuttner calls them, drew the reins around government spending fairly tightly and pulled them back just as soon as the serious hawks and the Obama haters shouted “boo.” This time, with a re-election obsessed, debt-ridden real-estate developer at the helm, the coronavirus consensus is “Spend, Spend, Spend,” as I wrote recently in Dollars&Sense. It is reasonable to ask, how long will these neo-Keynesian “foul-weather friends” support the needed massive deficit spending on this crisis? And looking ahead, will they try to pull the reins back in on other major social needs, including the fight against climate change?

More importantly, hawks aside, what is the right way for the U.S. to think about these questions? How big can deficits be? For how long can they continue? And for what purposes should they be incurred?

We can start by looking at the evidence. The definitive empirical analysis bearing on these questions is the work of my colleagues Michael Ash, Deepankar Basu, and Arin Dube.

Building on the critique of “the public debt cliff” by Thomas Herndon, Michael Ash, and Robert Pollin, they rigorously analyze data on public debt and economic growth for 22 developed countries from roughly 1880 until 2011. They assessed the claims in a number of research papers that high debt has a negative impact on the rate of economic growth. They also assessed the claim that there is a debt cliff, when government debt gets to around 90-100 percent of GDP, above which economic growth will take a big dive. But, in fact, the authors find no sizeable negative relationship in the full sample extending as far back as late 19th century. Moreover, they find no cliffs at all. And most relevant, they find that in the recent period, since 1970, “The relationship between government debt and economic growth is essentially zero.”

In short, the claim that high levels of government debt cause catastrophic economic outcomes simply lacks evidence.

Does this mean that for rich countries, the sky is the limit for government debt? Not necessarily. The highest ratio of debt to GDP in their data set is around 160 percent. What if debt levels go much higher outside of this range? The historical data cannot really tell us the answer. This is one reason we need to consider other factors specific to the situation at hand. These cross-country empirical studies necessarily mask specific conditions such as the cause of the debt accumulation and the domestic and international context.

The current specific environment in the U.S. is well narrated by The Financial Times quotes at the top. These are the conditions that most Keynesian economists agree can lead to benign large deficit spending for a significant period of time. When inflation is under control and relatively low, there is excess capacity in the economy or resources that can be reallocated to more productive ones, such as health care; the interest rates at which governments can borrow are well below the returns that society will get from government-spending programs; and the financial assets that the government issues to pay for these activities, be it money created by the Federal Reserve or debt (like government bonds), are in sufficient demand around the world that they will not be dumped in response to the attempts by the government and the Fed to send even more of these financial instruments into the portfolios of the world’s banks, governments, households and markets.

But none of these conditions are necessarily forever. Will investors and governments around the world be willing to accumulate and hold on to more and more U.S. dollars and dollar denominated IOUs? To be sure, the U.S. dollar is currently the dominant international currency and during crises, such as this, the global demand for dollars soars. But as the final FT quote above suggests, this is not necessarily permanent. China is working hard to make the renminbi a major key currency; and continued fumbling by the Trump administration on the global stage is giving them more and more opportunities to succeed.

Low interest rates, moreover, are not permanently feasible in the absence of strong financial market regulations. Combined with weak regulation, low rates eventually lead to financial crisis, as the current corporate-bond meltdown shows. And low inflation is not a permanent feature of capitalist economies. Shortages associated with climate change–induced droughts and food-production problems, among other factors, are bound to impact inflation over the coming decades. Higher and variable inflation can be managed but does impact the ability of financial markets to absorb low yield instruments such as money, and low interest government securities.

The need to take into account such situational factors when analyzing policies such as deficit spending constitutes a major difference between my perspective on how to analyze deficit spending, and the positions sometimes taken by Modern Monetary Theorists. What determines how big deficits can be and for how long requires close situational analysis, and cannot be inferred from first principles as MMTers try to do.

But, perhaps more important, issues of financing and full employment are not the only important potential constraints on spending. Even if had a lot of excess capacity, and even if the Fed could print as much money as it wants, it would still matter crucially what the government spends these dollars on. That is because, among other matters, unlike in Keynes’s time, we are now faced with a binding carbon budget, a climate change imperative. Now, free-lunchism doesn’t work, even from a Keynesian perspective.

That is why the question Kuttner asks about the amount of stimulus we get from different kinds of spending and tax cuts is not really the right question now. In the face of the pandemic, and in the grip of an ever-worsening climate crisis, we need to be talking not about a stimulus program, but rather a social protection and green transformation program. As my colleague James Crotty has shown in his masterful book on Keynes, Keynes Against Capitalism: His Economic Case for Liberal Socialism, even during the Great Depression, Keynes’s central argument was that in order to deal with the economic, social, and political crisis at hand, public spending and central bank policy needed to be directed not only at full employment, but, even more importantly, toward the social control and allocation of credit and investment to transform the British economy so it could meet the challenges of a new epoch.

In short, it matters enormously what we spend these trillions of dollars on. Simply insisting that we can do it without the bond-vigilantes getting us doesn’t get us far enough anymore.

Gerald Epstein is professor of economics and co-director of the Political Economy Research Institute at the University of Massachusetts Amherst and author, most recently, of The Political Economy of Central Banking: Contested Control and the Power of Finance (Elgar Press, 2019).