This is part of our economists roundtable on the corona crisis.

Robert Kuttner is right that a growing share of economists is (finally) getting more evidence-minded about the effect of public debt. These economists have seen that the large increase in the ratio of debt to GDP in the past decade failed to boost interest rates or inflation much at all. From this they have drawn the correct inference that rapid debt reduction should not be on the short-term priority list. But too few have addressed the question of why growing debt hasn’t pushed up interest rates or debt. This might be because the answer takes one out of politics-free observation: It’s because of rising inequality and the policy failure to stem it.

To understand inequality’s role in breaking the link between rising debt and interest rates or inflation, start with a generally-accepted point: All else equal, rising public debt should boost the growth of aggregate demand (spending by households, businesses and governments) relative to the economy’s productive capacity. But if the last decade’s rise in debt hasn’t budged interest rates or inflation, then the clear implication is that the economy is suffering from a chronic shortfall of demand even in the face of rising debt.

Most economists recognize that demand shortfalls can exist; recessions are just particularly serious demand shortfalls. But a generation of macroeconomists assumed these shortfalls were temporary and easy-to-fix, and that the much more pressing problem that policymakers would have address was a supply shortfall that spurred inflation or rising interest rates. Hence, for example, the Federal Reserve adopted a generations-long itchy trigger finger on interest rate increases to fight potential inflation, keeping labor markets too soft to give typical workers the labor market leverage they needed to spur reliable wage growth.

Some economists have certainly noted that this chronic shortfall in demand is the reason why growing debt hasn’t led to rising interest rates, and this has been a big analytical leap forward. But why this demand shortfall emerged and persists will require more leaps. Two key reasons (if not the only ones) include the policy-driven assault on the labor market leverage of typical workers that has been the root cause of the rise in market-income inequality, and the failure of our tax-and-transfer system to respond to this rise in market income inequality with progressive tax increases or more redistributive spending. These two “whys” are essentially the story of how inequality happened and what fiscal policy did not do to check it.

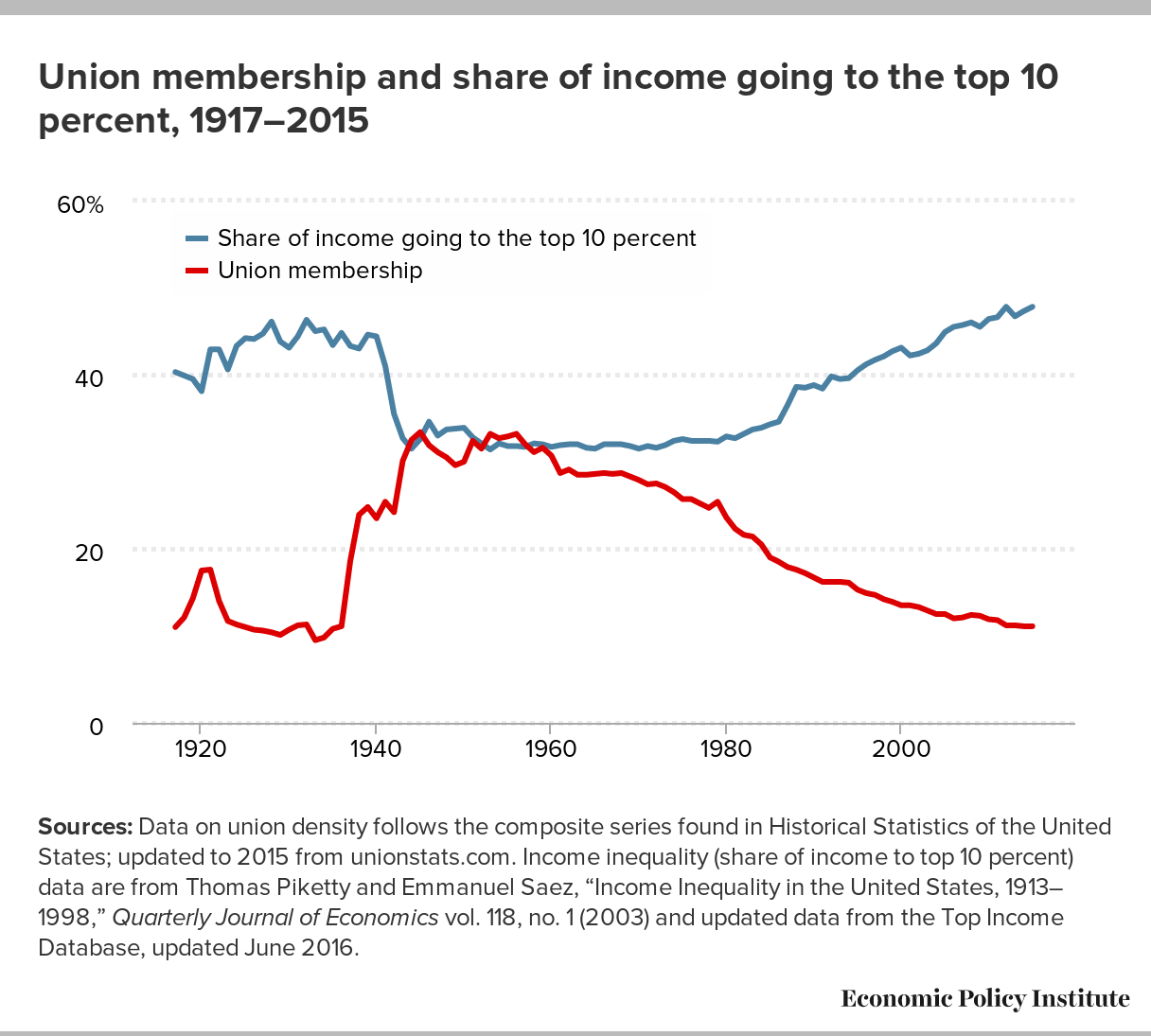

As inequality rose, more and more income was redistributed to the top, where households save a lot more than their low and middle-income peers. For a while we could maintain demand growth in the face of this steady upward redistribution by lowering interest rates and spending out of the occasional asset-market bubble fueled by private debt. But now we’re firmly in a world where interest rates can’t lift off much beyond zero without sacrificing any serious chance at reaching full employment.

Given this inequality we’ve generated over the past generation of economic life—and the demand shortfall that accompanies it as a result of the higher savings rate of households on the winning end of this rising inequality—the only way to sustain full employment going forward is to rely more on larger federal budget deficits. And if the choice is higher deficits with full employment versus lower deficits without, it’s clear that the best choice is to bring on the deficits. But this also means that anybody determined to slow debt growth needs to come with a plan to lower inequality and hence generate more private-sector demand growth.

Somewhat ironically, one sure policy path that would allow full employment to coexist with smaller deficits would be to increase spending on social insurance and safety net significantly while raising progressive taxes even more. This would result in a smaller deficit, but the progressive redistribution would boost demand growth by more than the slower debt growth reduced it. This path of increasing spending and taxes, leaving government bigger but deficits smaller, would not only be a solid economic strategy, it would also provide a pretty good test for whether it’s the size of the debt or the size (and progressivity) of government more generally that is the real worry for self-professed fiscal hawks.

A complementary plan to reduce inequality and hence allow lower deficits to co-exist with full employment is pursuing measures to boost U.S. workers’ leverage in labor markets. On the face of it, restoring the effective right to bargain collectively might not seem like a fiscal issue, but, the assault on this right has had profound effects on American inequality, and it would be far easier to significantly reduce debt ratios while maintaining full employment if this distribution of market income was much more equal. Again, anybody who seriously wants smaller deficits and full employment needs to think about how to reduce inequality—and boosting the labor market leverage of typical workers is a key tool for this effort.

{kind=link}

In the end, discussions about the proper level and trajectory of public debt cannot be divorced from other developments in the economy. There have been historical episodes across countries when economic growth really was constrained by the supply side, and running large fiscal deficits really would have put upward pressure on interest rates or inflation. But growth in the modern and unequal United States has been demand-constrained for at least a couple of decades now. Given this, rising debt not only does no harm, it actively boosts growth.

We should be really clear that the observation that raising debt in our demand-constrained economy is good for growth is not really anything to cheer. In fact, every year that we allow economic growth to be demand-constrained is another year of waste. We know, pretty clearly, how to solve demand constraints: use more debt used to finance demand-generating spending until we finally reverse the huge rise of inequality. But we haven’t yet found the political will to do it, and so the waste continues.

We should also be clear that there is no problem-free world in economic policymaking. Even if we managed to achieve a lot less inequality, faster demand growth and slower-growing public debt, policymakers will face problems, just different ones. For example, the phantom problem of recent decades—upward pressure on interest rates and inflation— would become real. The standard playbook for addressing these problems has been to rely on the Federal Reserve to bludgeon labor markets with higher interest rates and unemployment. We can do much better than that, using bargained wage restraint and incomes policies to slow inflationary pressure. But I would trade the problem of how to control too-fast demand growth for our current demand stagnation in a heartbeat. This trade would at least mean we’ve solved the infuriating political failure that kept us from addressing the easily solvable demand shortfall that has hampered growth for far too long.

Will the recent crisis somehow illuminate a path out of this political failure? It’s possible. At a minimum, the crisis highlights some crucial downsides of weak public investment and social insurance, and, it should have helped many recognize that lots of work that is currently low-wage is extremely high-value. Maybe this is a good start for a new conversation on all these issues.